Flood insurance has become one of the most important conversations in Tampa Bay real estate. As waterfront values continue to rise and homeowners reassess storm risk after recent hurricane seasons, many buyers and sellers are exploring alternatives beyond traditional FEMA-backed policies.

In 2026, private flood insurance is becoming increasingly common across Tampa Bay, especially among luxury homeowners seeking broader coverage, higher policy limits, and more flexible underwriting. From Snell Isle and Shore Acres to Davis Islands and Belleair Beach, affluent buyers are asking more detailed questions about flood zones, premiums, deductibles, and long-term insurability before making purchasing decisions.

For homeowners navigating the Tampa Bay housing market in 2026, understanding private flood insurance options is no longer optional. It is becoming a critical part of protecting real estate investments and maintaining affordability in coastal communities.

The Tampa Bay housing market in 2026 continues to experience a transition toward a more balanced market with increasing inventory and longer market times across Hillsborough and Pinellas counties. At the same time, flood insurance costs remain one of the largest variables impacting monthly ownership expenses.

Buyers are spending more time evaluating total ownership costs, and flood insurance has become one of the most heavily scrutinized line items.

In luxury waterfront neighborhoods, annual premiums can vary dramatically depending on:

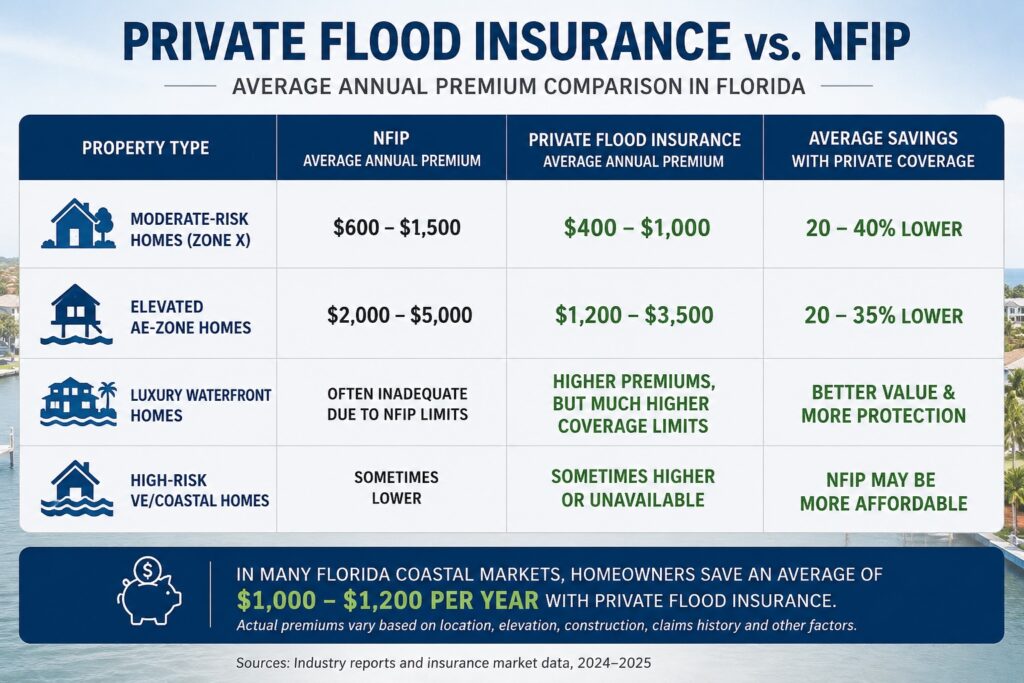

Many Tampa Bay homeowners are now comparing private flood insurance policies alongside traditional NFIP coverage to determine the best long-term value.

Private flood insurance refers to flood coverage provided by non-government insurance carriers rather than the National Flood Insurance Program (NFIP).

While NFIP remains the most recognized option, private insurers have expanded significantly across Florida over the last several years.

Private flood insurance policies may offer:

This has become particularly attractive for luxury homeowners in Tampa Bay where property values frequently exceed NFIP maximum coverage limits.

Luxury buyers in Tampa Bay are often purchasing properties well above NFIP structural coverage caps. Many waterfront homes in neighborhoods like:

require significantly higher dwelling limits than federal programs provide.

Affluent homeowners are increasingly prioritizing:

For buyers with substantial investments in interior finishes, detached structures, pools, docks, and landscaping, private policies may provide broader protection.

Here are several private flood insurance providers commonly used in Florida and the Tampa Bay area:

Private Flood Insurance Company | Website |

Neptune Flood Insurance | |

TypTap Insurance | |

Kin Insurance | |

Wright Flood | |

Better Flood Insurance | |

Aon Edge Flood | |

Superior Flood Insurance | |

Assurant Flood Solutions | |

Chubb Flood Insurance | |

PURE Insurance | |

Vault Insurance | |

Selective Flood Insurance | |

Lloyd’s of London Flood Programs |

Homeowners should compare:

Not every provider fits every property type, which is why many buyers work closely with specialized insurance brokers familiar with coastal Florida underwriting.

Flood insurance costs now directly influence buyer behavior in many coastal neighborhoods.

In some cases:

At the same time, well-positioned homes with favorable flood policies often stand out more aggressively in today’s market.

The Tampa Bay housing market 2026 reflects this growing emphasis on risk-adjusted value.

Properties featuring:

are increasingly viewed as premium assets.

Whether reviewing an existing policy or evaluating new coverage options, Tampa Bay homeowners should ask the following questions about flood insurance:

Flood zones significantly impact insurance pricing, lender requirements, and long-term resale value.

Many homeowners discover their existing policy limits may not fully cover rising construction and material costs.

Elevation certificates can dramatically influence premiums and may help qualify for lower rates.

If a home has flooded before, private flood carriers will usually look at:

Multiple flood claims become more difficult to get private flood insurance.

Some homeowners may qualify for broader coverage or better pricing through private flood insurers. Prior flood claims can affect future premiums, underwriting eligibility, and available carrier options.

Features such as:

may improve insurability and reduce costs.

Not all policies cover the full replacement cost of the structure or personal belongings.

Lower premiums sometimes come with significantly higher deductibles during a flood event.

Some private flood insurance policies include additional living expenses if the home becomes uninhabitable after flooding.

Because Florida’s insurance market changes rapidly, homeowners should regularly compare NFIP and private flood insurance options to ensure they receive the best available coverage and pricing.

Florida’s insurance landscape continues evolving rapidly, and flood insurance will remain a major topic for homeowners, investors, and real estate professionals.

The Tampa Bay housing market 2026 is increasingly shaped by:

However, Tampa Bay remains one of the most desirable coastal markets in the country because of:

Savvy buyers are not avoiding waterfront real estate. They are simply becoming more educated and strategic.

The Tampa Bay housing market in 2026 continues evolving, and flood insurance is now part of every serious real estate conversation.

Private flood insurance has opened new opportunities for homeowners seeking:

As buyers become more informed, homes with strong insurability profiles may continue outperforming competing properties.

Whether you are purchasing a waterfront estate, selling a luxury property, or evaluating long-term ownership costs, understanding flood insurance options is essential in today’s market.

At The Tenpenny Collection, we can connect you with trusted local insurance providers to help you understand your options and save you money. Contact us today for more information.