When the Federal Reserve gets a new Chair, headlines immediately begin predicting what will happen next for mortgage rates, home prices, and the housing market.

Some experts claim rates will fall. Others warn inflation could rise again. Buyers wonder if they should wait to purchase a home, while sellers try to determine whether demand is about to improve or weaken.

But historically, how much power does a Fed Chair actually have over real estate?

The answer is more nuanced than most headlines suggest.

A Federal Reserve Chair can influence economic conditions, investor confidence, and monetary policy direction. However, housing markets typically respond to broader economic forces such as inflation, employment, bond markets, consumer confidence, and housing supply.

In other words:

Fed Chairs do not directly control the housing market. Their policies influence the economy, and the economy influences housing.

That distinction matters as Jerome Powell officially stepped down from the chair position when his second term ended on May 15, 2026. Kevin Warsh has been confirmed as the new Federal Reserve Chair. So, what’s next for the residential real estate market under a new Fed Chair?

One of the biggest misconceptions in real estate is that the Federal Reserve directly sets mortgage rates.

It does not.

The Fed controls the federal funds rate, which affects short-term borrowing between banks. Mortgage rates, especially 30-year fixed rates, are influenced more heavily by:

This is why mortgage rates sometimes rise even when the Fed pauses rate hikes, and sometimes fall before the Fed cuts rates.

The Fed Chair still matters because the position shapes:

Financial markets often react to what the Fed signals almost as much as what it actually does.

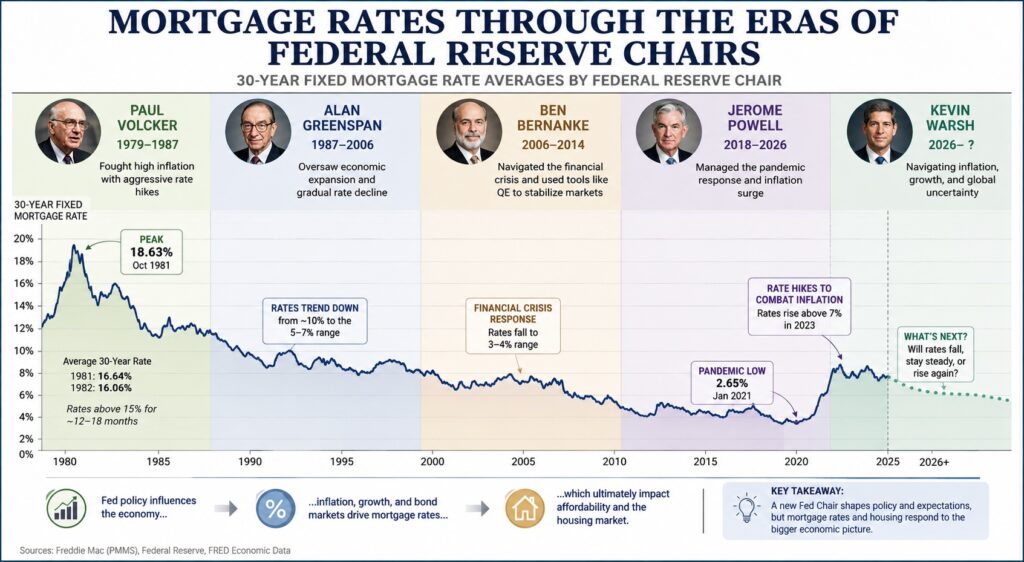

Historically, Federal Reserve Chairs have influenced housing indirectly through economic policy rather than by targeting real estate itself.

Volcker inherited severe inflation during the late 1970s. To slow inflation, the Fed aggressively raised interest rates.

Mortgage rates eventually exceeded 18% in 1981, the highest levels in modern U.S. history.

Mortgage rates remained above 15% for roughly 12 to 18 months during the early 1980s. Annual average 30-year mortgage rates were:

Volcker did not target housing specifically. His policies targeted inflation across the broader economy.

Housing slowed because:

The housing impact was a downstream effect of broader economic tightening.

Greenspan oversaw a long period of economic expansion and gradually declining interest rates.

Mortgage rates fell from roughly 10% in the late 1980s into the 5% to 7% range by the early 2000s.

Many economists later argued that rates remained too low for too long after the 2001 recession, helping fuel excessive borrowing and housing speculation.

However, the housing boom of the early 2000s was not caused by the Fed alone.

Other major contributors included:

Again, the Fed influenced economic conditions, but housing outcomes resulted from many overlapping forces.

Bernanke inherited the financial crisis and housing collapse.

The Fed responded by:

This was one of the few periods where the Fed more directly influenced mortgage markets.

Mortgage rates eventually fell into the 3% to 4% range.

Still, Bernanke’s primary goal was stabilizing the financial system and broader economy, not specifically boosting housing.

Housing recovered gradually because:

Powell’s tenure included two very different housing environments.

During COVID-19, the Fed cut rates aggressively and injected liquidity into financial markets.

Mortgage rates fell below 3%, fueling:

As inflation accelerated, the Fed raised rates aggressively to cool the broader economy.

Mortgage rates later climbed above 7%, sharply reducing affordability.

Again, the Fed was responding to economy-wide inflation pressures, not specifically attempting to slow housing.

This is currently the biggest question consumers are asking.

The honest answer is:

Not necessarily.

Mortgage rates are influenced more by:

than by one individual Fed Chair.

Some analysts believe Warsh may favor a more disciplined approach toward inflation and Federal Reserve intervention. He has previously criticized prolonged easy-money policies and excessive balance sheet expansion.

However, that does not automatically mean mortgage rates will rise or fall.

Markets are still focused primarily on:

This is why mortgage rates have not dramatically shifted simply because leadership changed at the Fed.

Yes. They could also fall.

That uncertainty is exactly why economists remain cautious about making bold predictions.

Some analysts believe mortgage rates could remain elevated if:

Others believe rates could gradually decline if inflation continues to cool and economic growth slows.

Importantly:

Mortgage rates do not always move in the same direction as the federal funds rate.

Even if the Fed eventually lowers short-term rates, mortgage rates may not fall substantially if inflation concerns remain elevated.

This is one reason many housing economists caution consumers against assuming that a new Fed Chair automatically improves affordability.

This question has become increasingly common as affordability challenges continue.

Historically, trying to perfectly time mortgage rates has been difficult.

Lower rates can improve affordability, but they can also:

Housing markets are driven by more than rates alone.

Buyers should also consider:

Many analysts caution against waiting solely for a major rate drop that may or may not happen quickly.

History shows that housing affordability depends on the combination of:

not simply Federal Reserve leadership.

At this stage, there is no objective answer.

Housing outcomes will likely depend more on:

than on personality differences between Fed Chairs.

That is historically consistent across multiple Federal Reserve transitions.

Volcker, Greenspan, Bernanke, and Powell each operated during dramatically different economic cycles. Their policies influenced housing indirectly because they influenced the broader economy.

Kevin Warsh now inherits:

How housing performs moving forward will depend less on the title of Fed Chair and more on how the broader economy evolves over the next several years.

Ultimately, the relationship between a Fed chair change and mortgage rates is more indirect than many headlines suggest. While Federal Reserve leadership can influence economic expectations and investor confidence, housing markets are still driven by affordability, inflation, inventory, and broader economic conditions.

History shows that Fed Chairs do not single-handedly create housing booms or crashes.

Instead:

That relationship is real, but it is indirect and often misunderstood.

As Kevin Warsh begins his tenure as Fed Chair, the housing market will likely remain focused on the same factors that matter most:

And as history has repeatedly shown, those forces usually matter more than any one individual at the Federal Reserve.

The housing market is confusing. Here is what we know from experience: following herd mentality never pays off. Identify your needs. How long will you own the house? Is it an investment property or a place you will call home? This matters.

If you need help analyzing today’s real estate market to determine if buying a home is right for you, contact The Tenpenny Collection for a consultation. Our goal is to help you make smart decisions.